Request a demo specialized to your need.

Developing a new medication is a tedious process and costs of clinical research are constantly on the rise. These are the two main reasons for the decreasing trend in the number of filings with the FDA. In the past ten years from 2003 to 2012, the average number of filings for novel drugs has decreased considerably from 30 to 26.

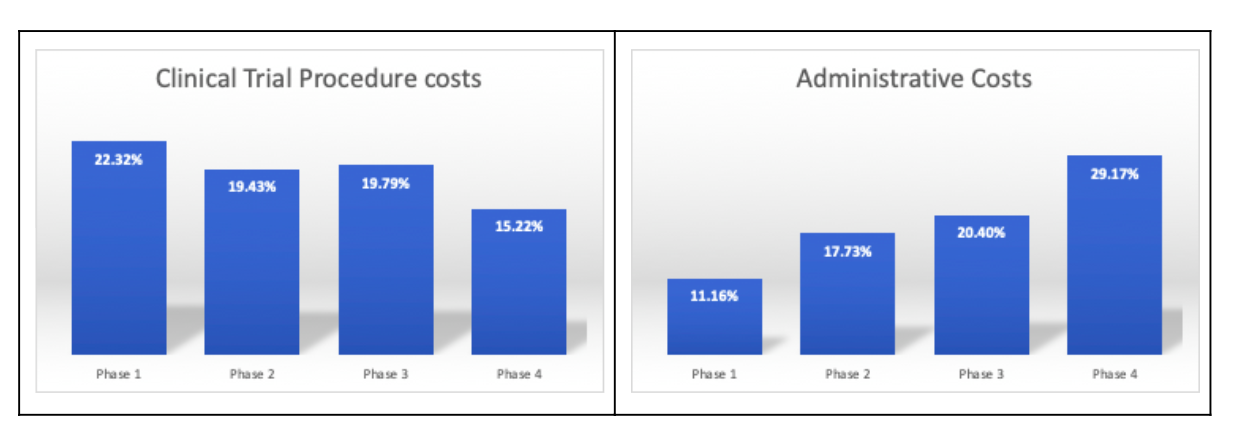

According to the U.S. Department of Health and Human Services (HHS), clinical trial procedure costs are the highest in the first three phases of the clinical study. Administrative costs are the highest in phase 4 studies. In most cases, companies face challenges in the initiation phases which are highly complex for planning and forecasting.

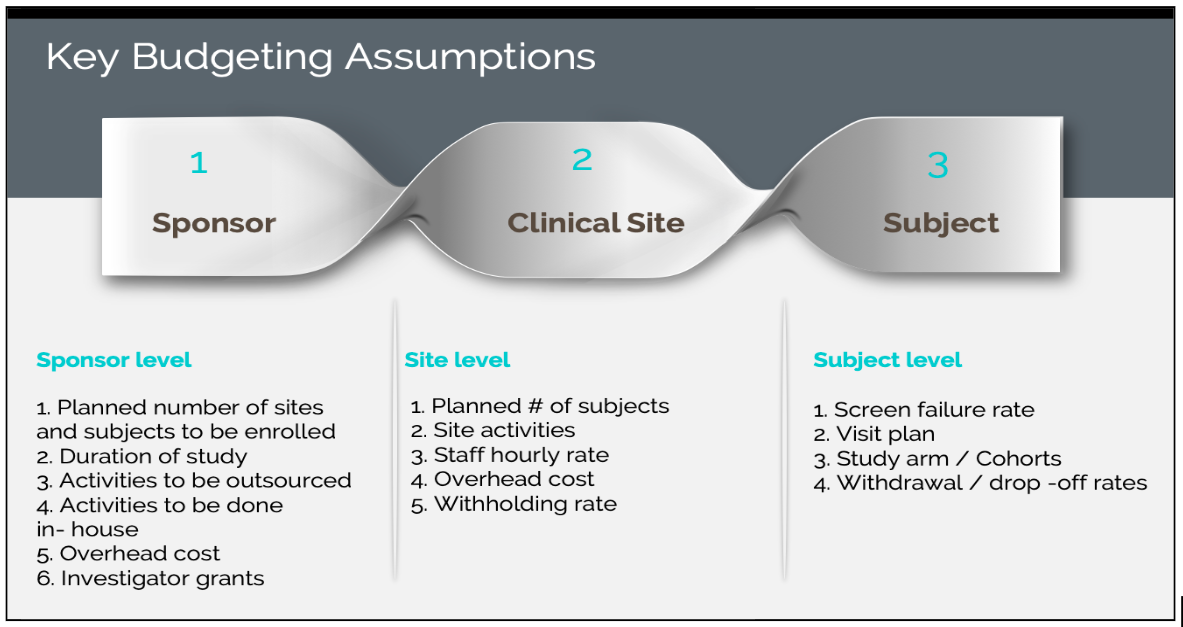

The key budgeting assumptions as per sponsor, clinical site, and subject:

Clinical Trial Budgeting is prepared in the planning stage prior to initiating the clinical study. The important aspect of how to do trial budgeting is the clear definition and consideration of all the assumptions and related costs. The budgeting costs vary based on the visit plan, the projected number of subjects to be recruited, the planned number of sites to be enrolled, the planned number of monitoring visits, the geographies in which the study is conducted, etc.

5 Best practices to consider in accounting to minimize variation in costs:

- The budget and payment schedule should account for patient retention rates to take into consideration the screen failures, patient withdrawal or deaths, loss to follow-ups, etc. during the trial process.

- Payments should be scheduled after the planned milestone completion and should follow a pattern with the timelines agreed upon by the sponsor and CRO’s.

- Administrative costs must be specified in detail and agreed upon by all stakeholders and in case of cancellation or termination of the study by the sponsor, the start-up and running costs will be payable.

- The standard procedure costs (commonly referred to as SoC- Standard of Care) are usually paid by the Insurance. Before planning for the budget the Investigator should be aware of all the expenses that should not be included in the budget.

- IRB fees are updated annually and vary depending on the region the institution is located. It is also based on activities such as review, amendment, etc. These have to be accounted for accordingly in the budget.

How can Cloudbyz Clinical Budget Management Solution (CTBM) benefit you?

One of the key challenges in clinical trial financial management is to properly account for all the multiple subject visits across clinical sites. Another important aspect is to minimize the challenges that arise with site payments, without error and delays. Cloudbyz CTBM addresses this challenge by a template-driven approach of visit plan management and using that to auto-create subject visits and subsequently auto-create payables based on completion of procedures and visits.

In Cloudbyz CTBM, the study and site level budgets are automatically linked and the appropriate rollup of budget and actuals happens seamlessly at line level and overall budget level. Once budgets are finalized, budget documents can be generated in the form of Excel or PDF and shared with other internal stakeholders like the finance and accounting department, etc. The solution supports versioning and a configurable approval process as well.

The solution also enables real-time collaboration between sponsors, CROs, and sites through secure investigator and sponsor portals.

References

https://www.cloudbyz.com/cloudbyz-ctms.html

https://clinicaltrialpodcast.com/ultimate-guide-to-clinical-trial-costs/

https://aspe.hhs.gov/report/examination-clinical-trial-costs-and-barriers-drug-development

Mythri Raghunandan

Clinical Research Specialist

Email: mythri.raghunandan@cloudbyz.com

Linkedin: https://www.linkedin.com/in/mythri-raghunandan-578605105/

Subscribe to our Newsletter